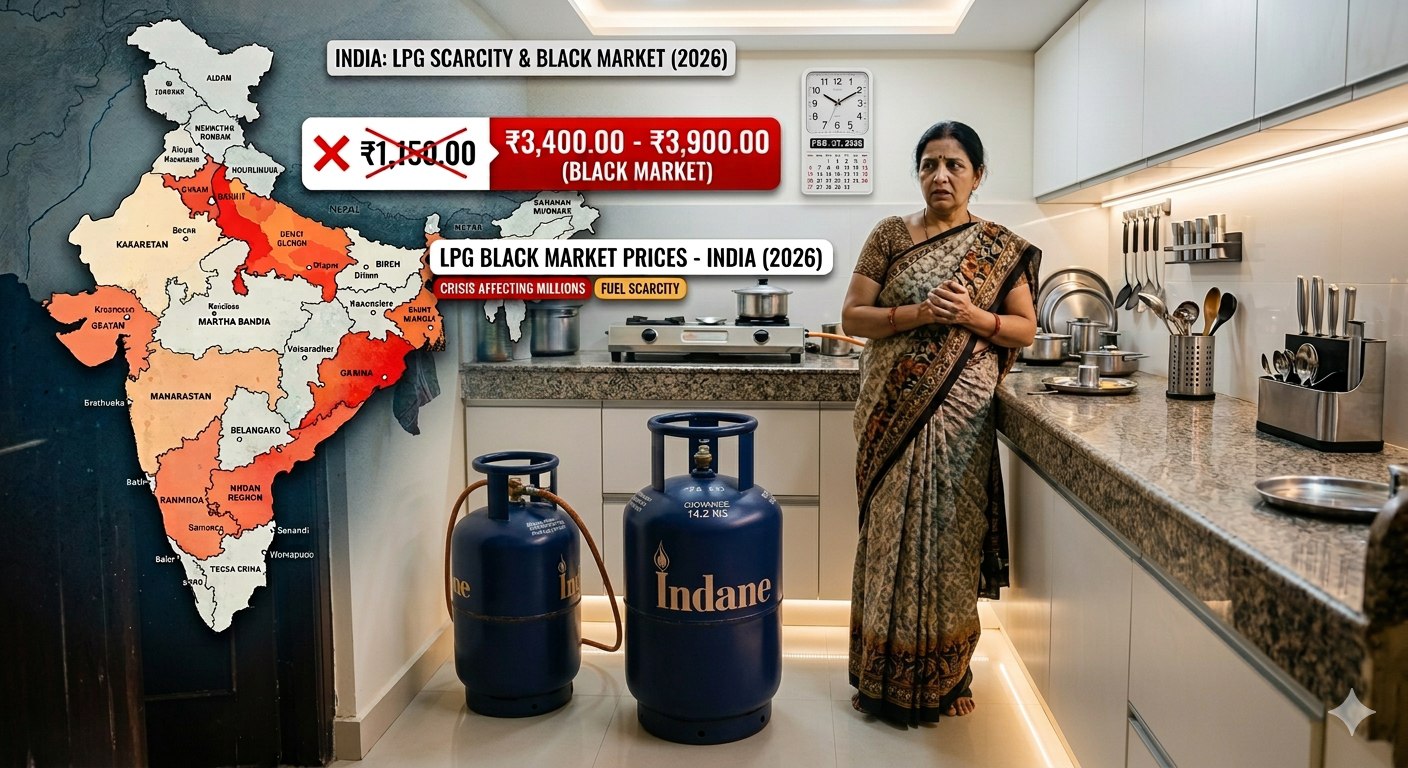

NEW DELHI: The continuing US-Israel-Iran conflict has begun to cramp India’s liquefied petroleum gas (LPG) trade, with city distributors reporting sporadic cylinder shortages and black-market prices in Delhi, Mumbai and Bengaluru touching ₹1 500–3 300 per 14 kg refill.

- Supply choke: At least two Very Large Gas Carriers scheduled to discharge in March have been diverted, traders say, trimming stocks at west-coast terminals.

- Price spike: Consumer retail remains capped, but informal quotes in Delhi have doubled; Mumbai street rates breach ₹3 000.

- School alert: Private schools in Delhi have advised parents to pack cold lunches "to mitigate lunch risk amid LPG shortage", according to circulars cited by parents.

The Ministry of Petroleum and Natural Gas has not issued formal supply curbs, yet city dealers confirm rationing.

"We are on 70% of normal quota and prioritising home consumers; commercial orders are back by two weeks."

— North India distributor

The Geopolitical Reality

Washington and Jerusalem’s expanded air campaign against Iran has pushed the Islamic Republic to threaten wider Strait of Hormuz disruption, the transit point for nearly one-fifth of global LPG and LNG volumes. Iran’s Revolutionary Guards have not mined the waterway, but war-risk premiums have added $8–10 per tonne to freight, making Middle-East cargoes costlier than Atlantic-origin lots.

Qatar, India’s dominant LNG partner, continues to load tankers, yet shippers are routing around the strait via the Cape of Good Hope, lengthening voyages by 18 days. Asia’s spot LNG price has risen 26% in two weeks; China, Thailand and Bangladesh are bidding aggressively, leaving marginal volumes for Indian importers.

Tehran’s announcement that it will open multiple fronts against US forces coincided with a claimed cyber strike on the US Army’s medical procurement portal, underscoring a shift to asymmetric retaliation that keeps energy choke-points under implicit threat.

The View from Delhi

India imports 56% of its LPG and 48% of LNG from Persian Gulf producers. New Delhi’s negotiating space is limited: Washington expects compliance with sanctions, Gulf suppliers demand premium pricing, and domestic prices are politically sensitive ahead of state polls.

Strategic stocks cover 18 days for LPG—below the 30-day norm—and fertiliser units depend on LNG feedstock for 45% of urea output. A prolonged shortfall therefore carries twin risks: household inflation and farm nutrient disruption, both politically combustible.

Delhi has invoked a 25% production hike at state refineries, but incremental domestic output is mainly propane-rich refinery gas, not the butane-rich mix required for household cylinders. Diversification to US or Australian LPG is feasible, yet the arbitrage window is narrowing as Asian buyers crowd Atlantic markets.

Strategic Implications

Energy security: India’s 2021 Hydrocarbon Strategy aimed to cut import dependency to 50% by 2027; the current squeeze highlights the urgency of accelerating exploration in the east coast Krishna-Godavari basin and fast-tracking the 5-mt/year Dhamra LNG terminal.

Price volatility: A three-month Hormuz risk premium could add $5–6 billion to India’s FY26 import bill even if crude remains range-bound. The immediate transmission channel is not petrol or diesel—those prices are insulated by Russian crude—but cylinder inflation could add 25–30 bps to CPI.

Diplomatic balancing: India abstained from the latest UNGA Iran resolution yet allowed the US Navy liaison officer to berth in Mumbai. Maintaining credible neutrality while safeguarding energy lanes will require quiet coordination with Oman and the UAE for alternate routing, and accelerated talks with Qatar for a long-term LNG peg indexed to Brent slope rather than spot JKM.

If hostilities extend beyond June, expect a cascading hit to fertiliser output just ahead of kharir planting. The resulting urea shortage would force either costly imports or subsidy overruns, complicating fiscal consolidation without breaching the 4.5% deficit target.